Hanoi office market sees stable performance despite Covid-19: Savills

The average gross rent decreased by a slight 1% on-quarter but increased 1% on-year.

Hanoi’s office market has yet to see significant negative impact of Covid-19 and maintained stable performance in the first quarter (Q1) of 2020, according to a Savills report.

| Hanoi office market posts stable performance in Q1/2020 |

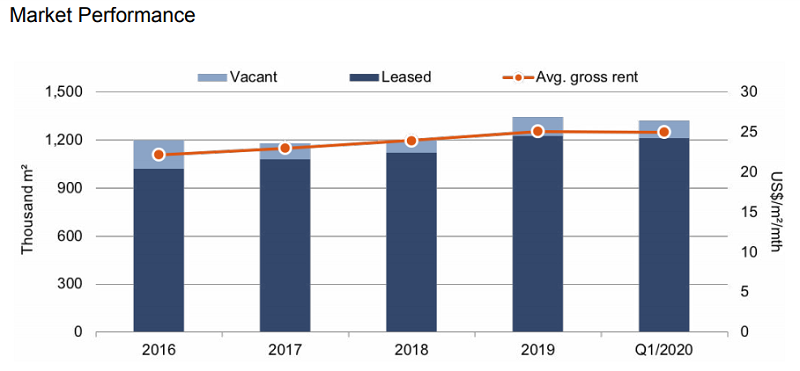

Total stock was approximately 1.8 million square meters (sq.m), down 1% on-quarter and up 3% on-year as two CBD Grade A projects International Centre and Vietcombank Tower were withdrawn for renovation and internal use.

Grade B continued to dominate the market with a 47% market share, followed by Grade C with 28%. Most projects are located in the West.

Q1/2020 take-up fell by 15,600 sq.m, the lowest in the past six quarters, mainly due to the closures of two Grade A projects. Highest take-ups were Grade B and the West; however, 2020 take-up will slow.

Most leases have terms of three to five years and so the cycle is smoothed. Rent was down across all grades. Occupancy was unchanged on-quarter and up one percentage point (ppt) on-year. Near-term vacancies will increase as tenants tightening spending, resize or close their offices, or put expansion plans on hold.

“Whilst the current office market remains healthy, there is a lag affect that may affect pricing in the future. Short-term discounts and healthy lessor/lessee partnering are now considered,” said Le Tuan Binh, head of Commercial Leasing, Savills Hanoi

| Hanoi's office market over the last years. Source: Savills Research and Consultancy |

Short-term impact

Covid-19 slowed Hanoi’s Q1/2020 GDP growth to 3.72% on-year, half of the same period last year (6.95%). Implemented FDI growth was 3.9% on-year, tremendously lower than in Q1/2019 (24.7%) since projects by Chinese, Korean and Japanese investors confronted obstacles in commercial transactions and customs clearance.

Most companies are encouraged to work from home, either entirely or on a rotating basis, leading to temporary closures of numerous workplaces, directly affecting office leases.

Companies in transportation, tourism and hospitality are the most affected due to their high level of social interaction. Manufacturing and trading companies have reduced demand as

production and supply chain disruption are felt. Besides, professional service providers are reassessing workforces to minimize costs.

Companies in healthcare and insurance are thriving; their demand is high. ICT firms are also strong, since technologies to optimize remote productivity are expanding.

Co-working demand has dropped significantly as it is vulnerable to the pandemic, with short leases and open plan spaces.

It is expected to recover quickly with demand mainly from small and medium-sized enterprises (SMEs).

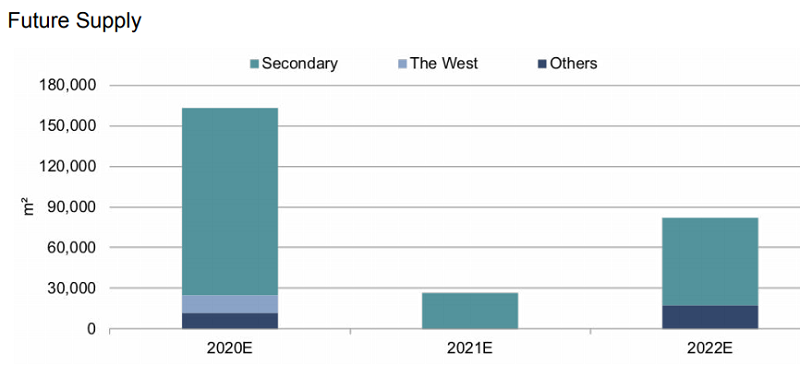

| Future supply of Hanoi office market. Source: Savills Research and Consultancy |

Rent adjustment

Landlords of low-grade buildings have responded quickly with rent adjustments. Concessions need to be made for a win-win solution that could include rent reductions, favorable lease terms, and renegotiation of essential clauses. There is also the option to ‘blend and extend’ to risk share and lengthen the original lease term for a stronger covenant with the landlord.

Promising future

Although Vietnam’s Q1/2020 GDP growth was the lowest in a decade at 3.8%, the economic outlook is still optimistic.

Governments and central banks have been responding to the situation with policy measures and financial aid to mitigate the economic impact. Vietnam is one of the global top 20 fiscal stimulators, with measures such as a credit package of VND250 trillion (US$10.86 billion) with preferential interest rates, the postponement of VAT, corporate income tax and land rent payments for up to five months without penalties, the temporary payment suspension of social insurance fund and union fees until June 2020, or longer depending on the outbreak.

These initiatives help to reduce immediate costs to maintain business continuity and preserve jobs.

A new wave of startups may enter the market following the pandemic, sparking fresh office demand.

Changing demand

External shocks do not immediately signal lease breaks or reductions, this is more likely at contract expiry. The crisis is possibly delivering us the most comprehensive home-office experiment in history.

Work-from-home may never replace offices completely, but the upcoming tech-boom will enable it further. There may be a reduction of CBD office demand as staff alternate between working in the office or from home.

In the long-term, despite a rebound in employment, future office areas may not increase in absolute proportion to the number of new hires.

The shift to flexibility drives continued growth in the shared office market. By 2024, millennials will constitute 75% of the active workforce. This growing group of office users prefers different offices. Options for working from home, office design and extra amenities are part of an attractive package.