Vietnamese manufacturing continues solid improvements

The bright spot in the latest PMI survey was employment, which increased at the fastest pace in three and a half years.

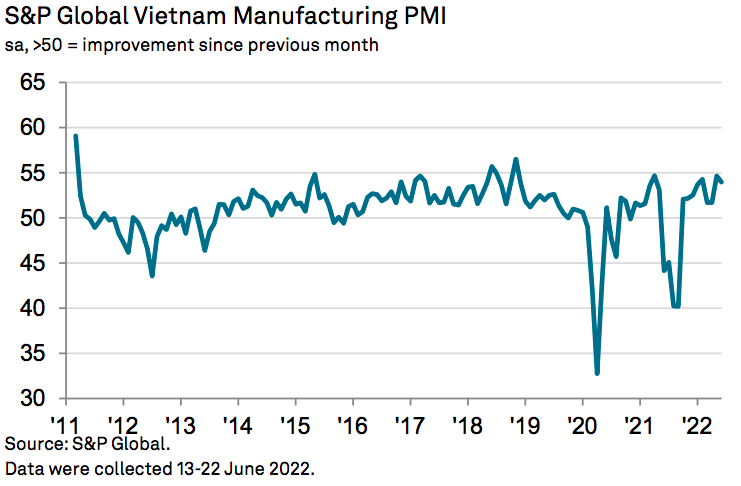

The Vietnam's Manufacturing Purchasing Managers' Index (PMI) posted 54.0 in June, down slightly from 54.7 in May but still signaling a solid monthly improvement in the health of the sector.

| Electronics production at Katolec Vietnam, Quang Minh Industrial Park, Hanoi. Photo: Pham Hung |

A reading below the 50 neutral marks indicates no change from the previous month or even contractions, and above 50 points means an expansion, according to S&P Global.

“The Vietnamese manufacturing sector ends the first half of 2022 in good health, with firms feeling that they've seen the back of the pandemic cane to generate new business at a solid rate,” said Andrew Harker, economics director at S&P Global.

"The main positive from the latest PMI survey was around employment, which increased at the fastest pace in three-and-a-half years. This shows that the difficulties firms were facing getting hold of staff around the turn of the year have eased, and means that manufacturers to respond quickly to customer requests and keep on top of workloads," he added.

Further marked increases were seen in both output and new orders at the end of the second quarter, as relative market stability due to a lack of pandemic disruption enabled demand to grow. Rates of expansion were particularly pronounced in the consumer goods category. Meanwhile, the growth of new export orders quickened to the fastest pace in four months, despite some reports that shipping difficulties had limited opportunities to export. Rising new orders encouraged manufacturers to expand workforce numbers again during June, extending the current sequence of increasing staffing levels to three months.

Furthermore, increased staffing capacity enabled firms to keep on top of workloads, with backlogs reduced for the second time in the past three months. Meanwhile, the shipping of finished items to customers meant that post-production inventories decreased again in June.

Input costs continued to rise sharply, with the rate of inflation quickening from that seen in May. A range of factors added to cost burdens, according to panelists, most notably higher gas and oil prices. Rising charges for shipping and freight and higher raw material prices were also mentioned. Higher costs for energy and shipping, in particular, were behind a further increase in selling prices. The rate of inflation softened, but was still marked and well above the average since the series began in March 2011. Continued supply-chain disruption was also a feature of the latest survey, although lead times lengthened to a lesser extent than in May. Where delivery delays were reported, firms linked this to Covid-19 lockdowns in mainland China, shipping issues, price rises, and material shortages. A further solid rise in purchasing activity was registered in June as firms responded to higher new orders. These purchased inputs were often used to directly support production, meaning that stocks of purchases continued to fall slightly.

Manufacturers expect the pandemic to remain under control, leading to stable market conditions and increasing production over the next 12 months. More than half of all respondents predicted a rise in output, with confidence above the series average.

Hanoi’s industrial production index of processing and manufacturing industries increased by nearly 7% during the first six months of 2022 compared to the same period last year, of which several industries achieved high growth rates, including paper production (up 20.3%), non-metallic mineral products (increased by 18.5%), prefabricated metal products (16.1%), wood processing and production (15.5%), among others. |