Vietnamese manufacturing sector predicted to grow in 2022

Employment rose for the first time in seven months as demand improves.

Vietnam’s firms remained optimistic that output will increase over the coming year, with sentiment ticking up since November on hopes that the Covid-19 pandemic will be brought under control over the course of 2022 and demand will strengthen.

| Sources: IHS Markit & Genernal Statistics Office of Vietnam |

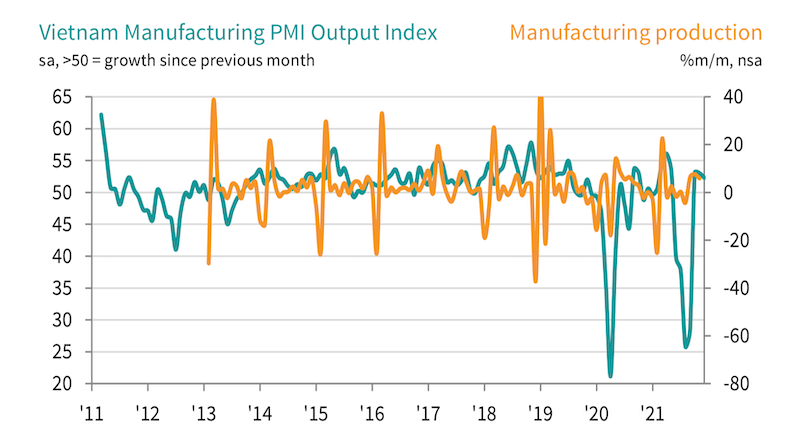

According to the latest study by IHS Markit, the Vietnamese manufacturing sector continued to grow at a solid pace at the end of 2021, and saw job creation resume following a sustained period of falling employment. Cost inflationary pressures remained marked, but eased notably since November, in part reflecting signs that supply-chain delays were becoming less pronounced.

The Vietnam Manufacturing Purchasing Managers’ IndexTM (PMI®) posted 52.5 in December, up from 52.2 in November and signalling a third successive monthly improvement in business conditions. Moreover, the solid strengthening in the health of the sector was the most marked since May.

Andrew Harker, Economics Director at IHS Markit, said the Vietnamese manufacturing sector ended 2021 in a steady growth phase. Client demand continued to improve in December, but the ongoing circulation of the Covid-19 pandemic is likely restricting the pace of the recovery.

“One positive from the latest PMI survey was that firms were finally able to start rebuilding workforces, albeit marginally, overcoming some of the difficulties attracting staff back to work following the recent wave of infections,” he added. “While firms were generally confident about the outlook for output in 2022, the new Omicron variant adds a further layer of uncertainty for the months ahead.”

A further solid increase in new orders was recorded at the end of the year, with the rate of growth broadly in line with that seen in November. The improvements in customer demand seen since the lifting of Covid-19 restrictions at the start of the final quarter of the year continued to fuel expansions in new business. New export orders also rose, with the rate of increase quickening to an eight-month high.

The rise in new orders supported a further expansion in manufacturing output, although the rate of growth slowed amid ongoing pandemic-related disruption.

There was positive news on the employment front at the end of the year as job creation resumed following six months of declining staffing levels. Higher output requirements and efforts to rebuild workforces following the recent wave of the pandemic were behind the increase. The rise in employment was only marginal, however, with some firms continuing to report that workers had returned to their hometowns and therefore weren't available.

Continued signs of labour shortages and new order growth combined to result in a further accumulation in backlogs of work. Outstanding business was up for the fourth month running, albeit at the slowest pace in this sequence.

A sharp and accelerated increase in purchasing activity was recorded in December as firms ramped up input buying in response to higher new orders and to attempt to build reserves.

Stocks of purchases continued to fall slightly, however, as inputs were largely used to support production.

Manufacturers continued to face delays in the delivery of inputs, but the rate at which lead times lengthened eased for the third successive month and was the weakest since April. There were some reports that the transportation situation was beginning to normalise but raw material shortages and shipping delays continued to hamper efforts to secure inputs.

Material shortages led to ongoing increases in input prices, while higher costs for oil and freight were also mentioned. However, the rate of input price inflation eased from that seen in November. Output prices also rose at a softer pace, albeit one that was still well above the series average.