Fintech is emerging as a driver of innovative financial solutions during Covid-19

Fintech – the fusion of finance and technology – could be a game-changer for inclusive economic growth amidst the pandemic.

Financial technology (fintech), or the fusion of finance and technology, has emerged as a new model for financial innovation. Fintech covers a constellation of complementary technologies—including mobile networks, big data, cloud computing, distributed ledger technology, artificial intelligence (AI), and data analytics—that jointly shape a broad swathe of operations in the financial industry.

| In India, mobile phones are being used to create “human ATMs” that provide greater access to fintech services. Photo: Ravi Sharma |

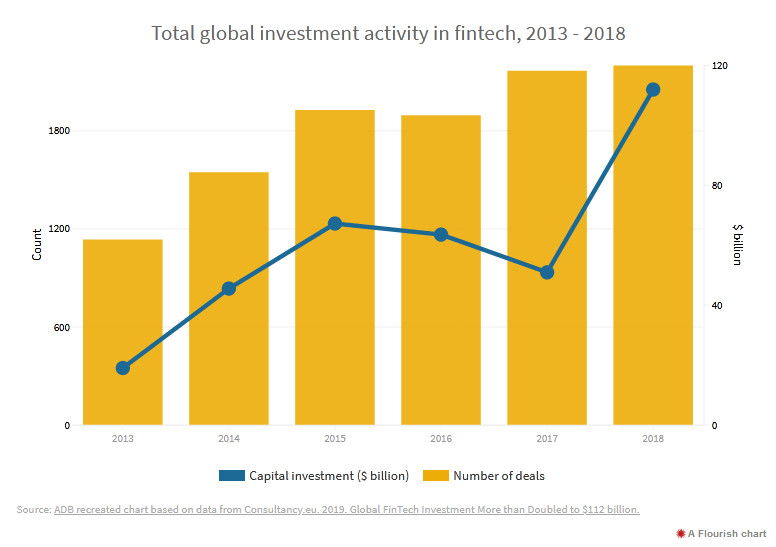

The past few years have witnessed the rapid growth of investment in fintech. It has already left its imprint on a wide array of financial services, including microfinance, blockchain, payments, personal finance, digital banking, insurance, wealth management, capital markets, money transfers, and mortgages.

Fintech enhances financial inclusion and broadens access to financial services by capitalizing on technological advances. It mitigates the risks and lack of information associated with underserved households and small and medium-sized enterprises (SMEs) via digital financial services and enhanced risk-assessment skills.

Specialized digital banking businesses serve specific sectors and demographic groups via business-to-consumer and business-to-business debit and credit extended to underbanked and unbanked individuals, households, and SMEs. In doing so, fintech not only improves the variety and efficiency of financial services, but also enhances financial inclusion. According to a recent ADB study, digital financial solutions can address about 40% of unmet demand for payment services and about 20% of credit requirements of poor households and small businesses in Asia.

Fintech’s role as a driver of financial inclusion is especially pronounced in financially underdeveloped emerging markets. A 2019 study documented a positive association between financial innovation and financial inclusion in a sample of six South Asian countries. A recent report from CB Insights shows that customers in emerging African markets have benefited from digital microfinance, especially mobile payments, microcredit, and saving accounts.

Around Asia, examples can be found of how financial inclusion can be promoted via fintech. For example, an AI-enabled credit score system supported by ADB helped more than 8,000 SMEs in the Greater Mekong Subregion obtain credit of $50,000 each through the end of March 2018. An ADB-backed cloud-based banking app in the Philippines and branchless banking in Indonesia have contributed to financial inclusion in member economies of the Association of Southeast Asian Nations. Asia is now a major player riding the global fintech wave, hosting 34 out of top 100 global fintech innovators at the end of 2019.

The role of fintech in improving financial inclusion comes to the fore during big economic shocks such as the Covid-19 pandemic. The poor suffer disproportionately during such shocks. Their hardship is exacerbated by lack of access to financial services, and they often do not have online bank accounts.

Even in advanced economies like the United States, delivering financial assistance to the unemployed and small businesses has emerged as a major problem during the pandemic.The nimbleness, flexibility, and contactless nature of fintech can facilitate social distancing. For example, on 14 April 2020, PayPal and other fintech companies in the United States were approved to participate in a government program to extend loans to small businesses.

The Covid-19 crisis creates opportunities to further expand the role of fintech in financial inclusion in developing economies. By extending financial services to vulnerable groups, fintech contributes not only to inclusive growth but also to the economic resilience of the poor and SMEs in times of economic shock.

Developing economies can harness fintech to keep the poor and SMEs connected to the financial system even in the face of crisis. In particular, fintech can efficiently unlock new sources of finance for vulnerable groups that are underserved by banks and other traditional financial institutions.

In developing countries in Asia, fintech companies are coming up with innovative solutions to fund SMEs struggling to stay afloat amid Covid-19. They are providing new turn-key loan origination and underwriting platforms to allow banks and lenders to provide financing for small businesses.

These platforms encompass risk assessment and insurance capabilities. Fintech also offers innovative finance solutions that are valuable to low-income groups during pandemics. For instance, the Indonesian ride-hailing delivery start-up Gojek offers a cash-in, cash-out platform for financial services. India’s Eko, a financial transactions platform, is trying to create “human ATMs” out of anyone with a mobile phone and a little cash.

While financial innovation promotes financial inclusion, it also raises regulatory challenges such as cybersecurity, other technical vulnerabilities, data governance, and privacy protection. At a broader level, regulators must strike the right balance between enabling fintech innovations that benefit the poor and SMEs while also monitoring and managing the risks associated with innovation.

Given the frenetic pace of innovation in the fintech sector, which is likely to pick up even more speed in the increasingly digital post-Covid-19 world, regulatory capacity must be strengthened to keep pace with change.

Finally, developing economies must make digital infrastructure investments to improve the interface between the digital and nondigital economies for the poor.

Authors:

Donghyun Park is Principal Economist, Economic Research and Regional Cooperation Department, ADB.

Shu Tian is Economist, Economic Research and Regional Cooperation Department, ADB.