Bond markets and borrowing: How Asia’s developing countries are managing the pandemic

The pandemic has shown central bankers and public debt managers that innovation and creativity are needed to maintain borrowing opportunities and keep local currency bond markets functioning.

Whilst the pandemic has rocked populations and health systems, it has also prompted unprecedented economic challenges and strains on financial systems, particularly in the developing world. Fortunately, central banks and finance ministries were prepared for remote working, having embraced vigorous business continuity plans, even though such arrangements were generally anticipated for short-term interruptions only.

The initial shock of the pandemic manifested in a flight to quality from investors, which eventually spilled over into a flight to cash as liquidity concerns grew. This meant that investors sold their emerging markets bonds and equities as they scrambled for safe-haven assets and even for hard cash as the worst fears materialized.

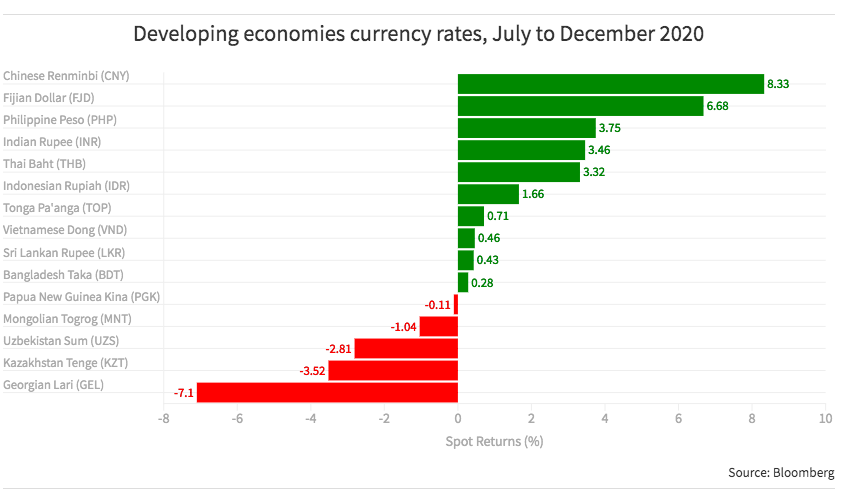

Foreign exchange rates are a reliable barometer of investor sentiment, and the severe gyrations witnessed in early 2020 suggested that emerging market carry trades were being hurriedly unwound. Fortunately, in some cases, the downside was reversed in the second half of the year.

In the bond markets, yield curves steepened as short-term interest rates fell, foreign investment withdrew, and domestic funds cut duration. But whilst central banks can control short-term interest rates, long-term yields are determined by the market, and they remained stubbornly high. This proved the case in India where the Reserve Bank conducted quantitative easing and cut the overnight reverse repo rate to 3.35%, while 10-year government bond yields remained around 6%. Inevitably, central banks also cut Reserve Asset Ratios in a concerted effort to pump liquidity into the financial system. Diversification trades simply did not work in this environment, with credit products gapping out in the absence of any buyers, thereby frustrating more recent reserve management strategies.

Over time, as governments rolled out counter-cyclical measures to protect employment and prop up their national economies, enormous challenges arose for public sector financing as tax revenues collapsed and borrowing programs multiplied. Both the income and expense sides of national accounts were hit simultaneously. Whilst developed countries took a digital leap forward in using e-payments, some developing countries even reported greater demand for physical cash, especially in US dollars, as confidence evaporated.

Targeted Covid-19 socio-economic strategies included the Philippines’ Four Pillars Policy, known as Bayan Bayanihan comprising emergency support for low-income households and SMEs; expanded medical resources; monetary action; and a job-creation recovery plan.

Kazakhstan continued to reform its defined contribution pension scheme (based on the Chile model and Singapore’s Central Provident Fund) to allow for early withdrawals to pay for housing and medical expenses from January 2021.

National borrowing programs were re-calibrated for much greater government spending, with Thailand doubling its funding needs from THB 1,163,835 million ($37.5bn) in 2019 to THB 2,327,214 million ($75bn) in 2021.

Job support subsidies were commonplace, but the balance of preventing the spread of the virus against maintaining economic momentum was – and still is - a universal challenge. Central banks from developing countries mostly do not enjoy access to currency swap facilities provided by the Federal Reserve, the Bank of Japan, or the European Central Bank, so reliance on concessionary finance lenders such as ADB and the World Bank has increased significantly.

Faced with multiple sovereign downgrades, investor appetite for emerging market hard currency debt quickly dried up as a consequence of the risk-off environment, with Indonesia, the Philippines, and the People’s Republic of China among the few developing countries able to borrow offshore in the middle two quarters of 2020. This paid testament to their regular dialogue with investors and established track record in the international bond markets.

Some developing countries in Asia continued to innovate in their financial markets during the crisis. Philippines and Thailand issued successful retail-targeted bonds, Thailand also emphasized a new environmental, social, and corporate governance (ESG) borrowing program, and Uzbekistan launched its first offshore currency linked sovereign bonds, garnering a vote of confidence from investors, albeit with a hefty coupon of 14.5% for three years.

Indonesia continued to issue green Sukuk, with a third $750 million 5-year offering completed in July 2020. Remarkably, Indonesia also completed a $5.2bn currency conversion exercise on its loans, re-balancing its foreign currency debt across EUR, USD, and JPY whilst simultaneously locking in ultra-low fixed rates of interest.

ADB continued to innovate in local currencies, launching maiden bond issues in Mongolian togrog and Pakistan rupees, green and gender bonds in Kazakhstan tenge, and new borrowings in Georgian lari and Indian rupees. ADB also issued its third panda bond, an RMB 2bn five-year offering, after a 12-year hiatus from the market, again underlining the importance of access to deep and liquid domestic capital markets.

The pandemic illustrated that central bankers and public debt managers need a consistent approach to investor relations to keep borrowing windows open. A well-functioning local currency bond market is also critical to the debt management strategy. Most importantly, the last year has shown us that innovation and creativity can still thrive in a pandemic.

Jonathan Grosvenor is ADB's Head of Treasury Client Solutions