Growing FDI commitments reinforce Vietnam investment competitiveness: WB

Close attention should be on the capacity of the Vietnamese economy to firm up its recovery from the coronavirus crisis, noted the World Bank.

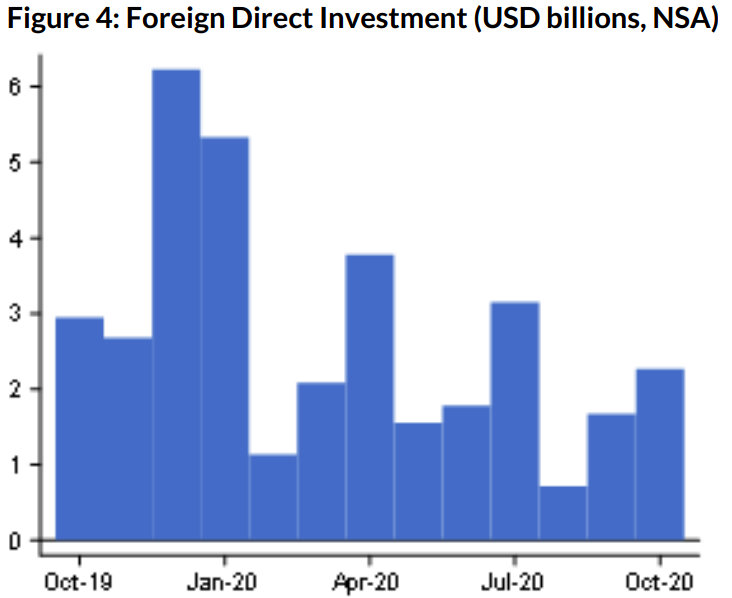

In the first ten months of 2020, Vietnam attracted US$23.5 billion of foreign direct investment (FDI), which about 19.4% lower than in the same period of 2019, but remains a remarkable achievement, given UNCTAD’s projection of 30-45% decline in FDI inflows to East Asia in 2020, according to the World Bank.

Source: WB report. |

As the second wave of coronavirus in Vietnam has been contained successfully, FDI rose to about US$2.27 billion in October, compared to US$1.67 billion in September and US$0.8 billion in August.

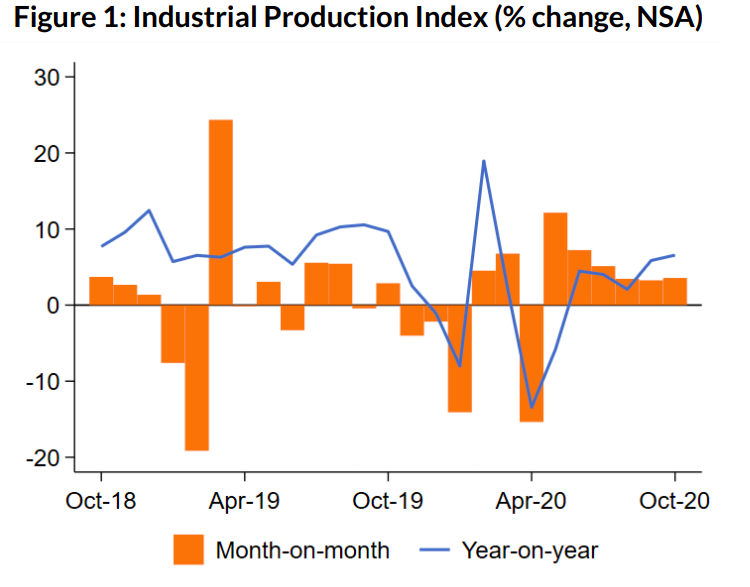

Meanwhile, recovery continued to strengthen in October, with manufacturing sector registering growth rate close to pre-Covid-19 period, noted the World Bank in its monthly economic report.

Both manufacturing and retail sales registered the highest growth rate year-on-year in October since the outbreak of coronavirus in February. The industrial production index and retail sales of goods increased by 6.6% and 6.7% year-on-year, respectively.

| Source: WB report. |

The country’s Manufacturing Purchasing Managers' Index (PMI), which measures the performance of the manufacturing sector and is derived from a survey of 400 manufacturing companies, was at 51.8 in October, where a reading above 50 indicates expansion of the sector.

Growth of retail sales is largely driven by domestic demand, while travel and tourism are not showing signs of recovery. Retail sales of goods was up 5.4% in the first 10 months of the 2020 compared to the same period last year.

On the other hand, domestic and international travel registered 30% and 80% drops respectively in the first 10 months of 2020 compared to the same period of 2019. International travels remain highly restricted, with the number of foreign tourists falling by 73.8% in the first 10 months of the year compared to the same period of 2019.

Build-up of record merchandise trade surplus continues

Vietnam’s merchandise trade surplus reached a record US$17.7 billion in the first 10 months of the year, bolstered by US$1.4 billion surplus in October

Compared to October 2019, merchandise exports and imports grew by 9.7% and 9.8% year-on-year, respectively. While exports of phones, textiles and apparel, footwear and agricultural products declined significantly, those of computers and electronics grew solidly amid the Covid-19 crisis.

Source: WB report. |

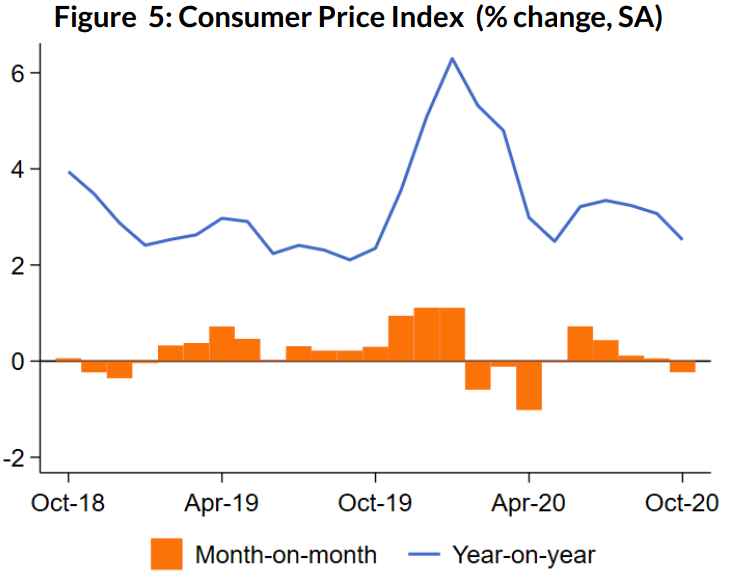

Inflation remains subdued

The October Consumer Price Index (CPI) remained flat compared to three previous months reflecting short term stability in the prices of food, energy, and transport. It was up 2.5% compared to October 2019, driven mostly by higher prices of food and catering services.

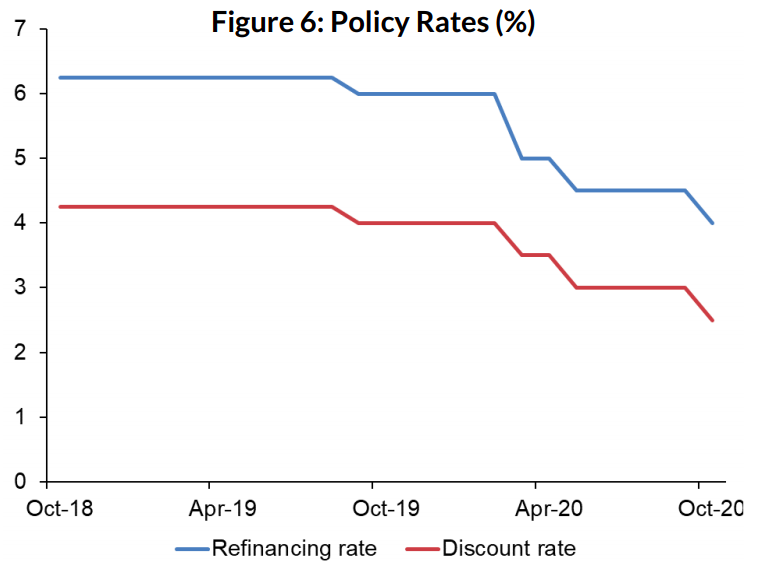

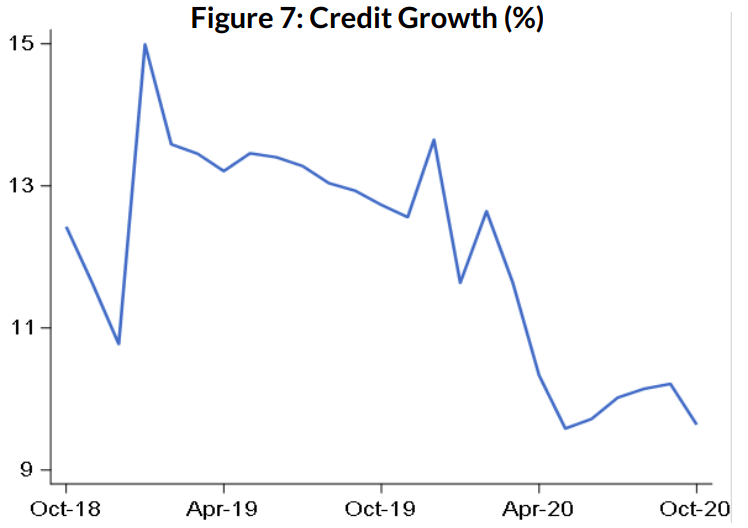

On the first of October, the State Bank of Vietnam (SBV) cut the refinancing rate from 4.5% to 4% and the discount rate from 3% to 2.5%. This move was aligned with the government’s effort to ease the cost of credit since the beginning of the Covid-19 crisis. However, credit growth remained slow at 9.6% in October year-on-year, slightly down from 10.2% in September and reinforcing the falling trend observed since 2017. Nonetheless, this growth rate is much higher than the nominal GDP growth, so that the credit/GDP ratio is still increasing.

Source: WB report. |

Public spending on the rise

The Covid-19 crisis has changed the course of fiscal policy. Total revenue in the first 10 months of 2020 declined by 10.3% compared to the same period in 2019 due to slower economic activities and tax deferrals to support companies.

In the meantime, total expenditures rose by 9.7% compared to the first 10 months of 2019. Particularly, public investment expenditure increased by 50.3%, thanks to the government’s efforts to accelerate disbursement, which stands at 68.3% as of October 2020 compared to 54.7% in October 2019.

| Source: WB report. |

Also, the severe damages unleashed by the October storms on Central Vietnam and the needed funds for assistance and reconstruction are expected to add pressure on the tightening fiscal space in the next few months, as economic losses from these tropical storms are estimated at VND29.3 trillion (US$1.3 billion).

The Vietnamese government has been able to finance the fiscal gap by using part of the reserves accumulated before the Covid-19 crisis. It has also continued to borrow on the domestic market for an amount of VDN260 trillion (US$11.21 billion) since the beginning of the year.

Looking ahead, close attention should be on the capacity of the Vietnamese economy to firm up its recovery from the coronavirus crisis, noted the World Bank.

On the one hand, near-elimination of restrictive and social distancing measures within the country as well as rising domestic demand fueled by higher public investment and easing credit conditions should stimulate domestic economic expansion.

On the other hand, the deterioration of the health and economic conditions in the rest of the world may affect Vietnam’s external sector. Also, severe life and economic losses due to the October storms highlight the need to make the economy and public finance more resilient to climate change, it added.