Moody's turns outlook of Mong Duong Finance to negative

The negative outlook on the rating mirrors the negative outlook on Vietnam's sovereign rating, given the government's commitment to MDP's power project.

Moody's Investors Service has confirmed Mong Duong Finance Holdings BV's (Mong Duong Finance) Ba3 USD senior secured notes rating, and changed its rating outlook to negative.

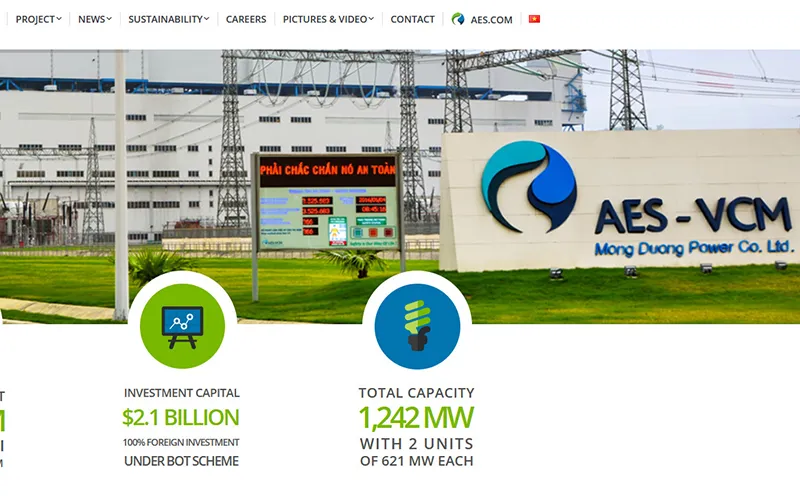

| A visual of the website of AES-VCM Mong Duong Power Company Limited |

The rating action on Thursday concludes the review for downgrade initiated on October 10, 2019, prompted by Moody's decision a day before to place the Ba3 local and foreign currency issuer and senior unsecured ratings of the Government of Vietnam under review for downgrade.

The rating action follows Moody's decision on December 18 to confirm Vietnam's Ba3 ratings with a negative outlook.

Mong Duong Finance is a finance entity whose credit profile is closely linked to AES-VCM Mong Duong Power Company Limited (MDP), because of several structural features.

MDP owns coal-fired power plants in Vietnam and operates with the assurance that the government will make reliable and timely payments to MDP, if and when required, under the Government Guarantee and Undertaking Agreement (GGU) and the Build Operate Transfer (BOT) contract.

“The rating action reflects the close links between MDP and the Vietnamese government, given that the government's commitment to MDP under the GGU and the BOT contract is a key driver for MDP's credit quality," says Mic Kang, a Moody's Vice President and Senior Credit Officer.

The government's commitment to MDP under the GGU and the BOT contract supports the predictability of the company's operating cash flow, while mitigating MDP's risk exposure to its single offtaker, Vietnam Electricity, and its sole coal supplier, Vietnam National Coal-Mineral Industries Group (Vinacomin).

Under the GGU and the BOT contract, the government guarantees the performance of all payment obligations and all financial commitments of Vietnam Electricity and Vinacomin, and compensates MDP for any operational difficulties stemming from a failure of coal supply by Vinacomin.

The negative outlook on the rating mirrors the negative outlook on Vietnam's sovereign rating, given the government's commitment to MDP's power project.

Moody's could revise the outlook to stable if (1) the outlook on Vietnam's sovereign ratings is changed to stable; (2) the government's strong commitment to MDP's power project remains intact and (3) MDP maintains its solid operations and financial leverage.

Moody's could downgrade the rating if (1) Moody's downgrades Vietnam's sovereign; or (2) MDP's debt service coverage ratio falls below 1.1x during the amortization period.

MDP is a limited liability joint venture that owns and operates two identical sub-critical coal fired power units with an aggregate net capacity of 1,120 megawatts. The units are located around 220 kilometers east of Hanoi (50 km north-east of Ha Long city in Quang Ninh province.

MDP is owned by AES Mong Duong Holdings B.V. (51%) - a subsidiary of AES

Corporation - PSC Energy Global Co., Ltd (30%) – a subsidiary of POSCO Energy, and which is in turn owned by POSCO – and Stable Investment Corporation (19%), which is owned by China Investment Corporation, a sovereign wealth fund of the Government of China.